At the 2025 Indonesia Mining Conference and Critical Metals Summit—2025 Southeast Asia Tin Industry Conference, hosted by SMM Information & Technology Co., Ltd. (SMM), supported by the Indonesian Ministry of Foreign Affairs as the government supporter, and co-organized by the Indonesian Nickel Miners Association (APNI), Jakarta Futures Exchange, and China Coal Resource Network, Mingfu Li, Director of Qiandao Metals Co., Ltd. in Gejiu City, shared insights on the topic "Analysis of Myanmar Tin Ore Supply Status and Policy Impacts."

Global Tin Ore Resource Distribution

Overview of Global Tin Ore Reserves and Production

According to USGS, global tin reserves in 2024 were 5.254 million mt, with the top five reserve countries mainly concentrated in China (19%), Indonesia (15.23%), Myanmar (13.32%), Australia (11.8%), Russia (8.76%), and Brazil (7.99%).

In terms of production, China (71,000 mt), Indonesia (52,500 mt), Myanmar (24,000 mt), Peru (33,000 mt), and the DRC (26,000 mt) accounted for a combined 71.64% of global production.

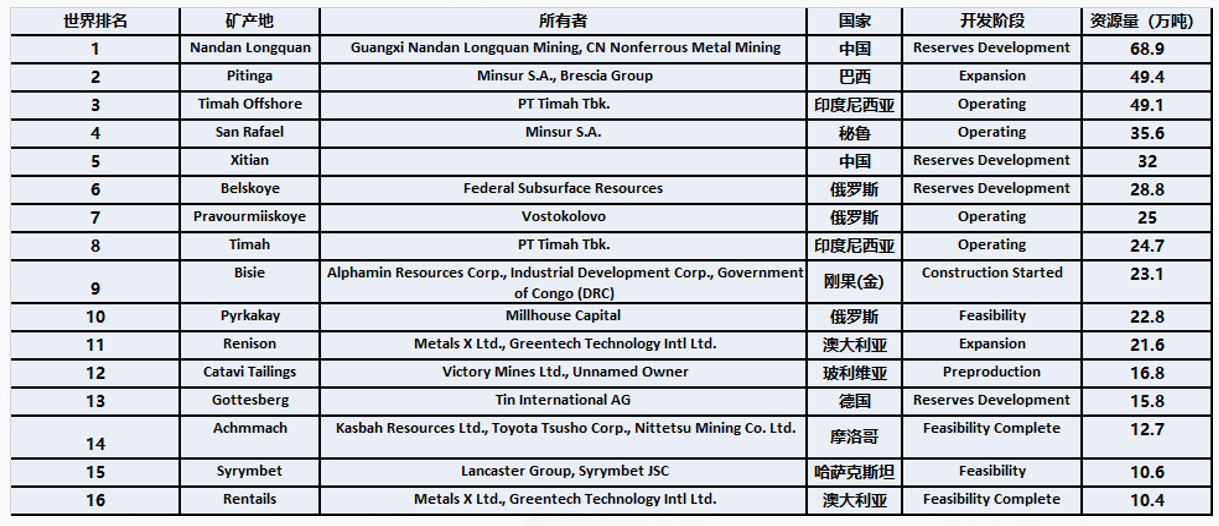

Tin Ore Resource Distribution

Currently, over 70 countries (regions) are engaged in the exploration, development, and utilization of tin ore resources. Globally, there are 218 tin mines, of which 61 mines have resources exceeding 10,000 mt, and 16 mines have resources exceeding 100,000 mt.

Major Global Tin Mines

The total resources of tin mines with more than 1 million mt globally amount to 4.47 million mt, accounting for approximately 40-50%.

Current Status and Development of Tin Ore in Myanmar

Wa State Resource Situation

The mineral resources in Wa State are roughly divided into three parts:

1. Nandeng Special Zone Gold Mine Area, the earliest discovered, with major minerals including zinc oxide, lead-zinc ore, and zinc sulfide, while other minerals are not of scale.

2. Longtan Mine Area, with major minerals being tin ore, lead-zinc ore, and gold ore.

3. Mansang (Bangka) Mine Area, currently the largest in scale, with major minerals being tin ore, lead-zinc ore, and Bangyang antimony ore. Among them, the Bangka tin polymetallic ore and Bangyang antimony ore are newly discovered mining areas in recent years.

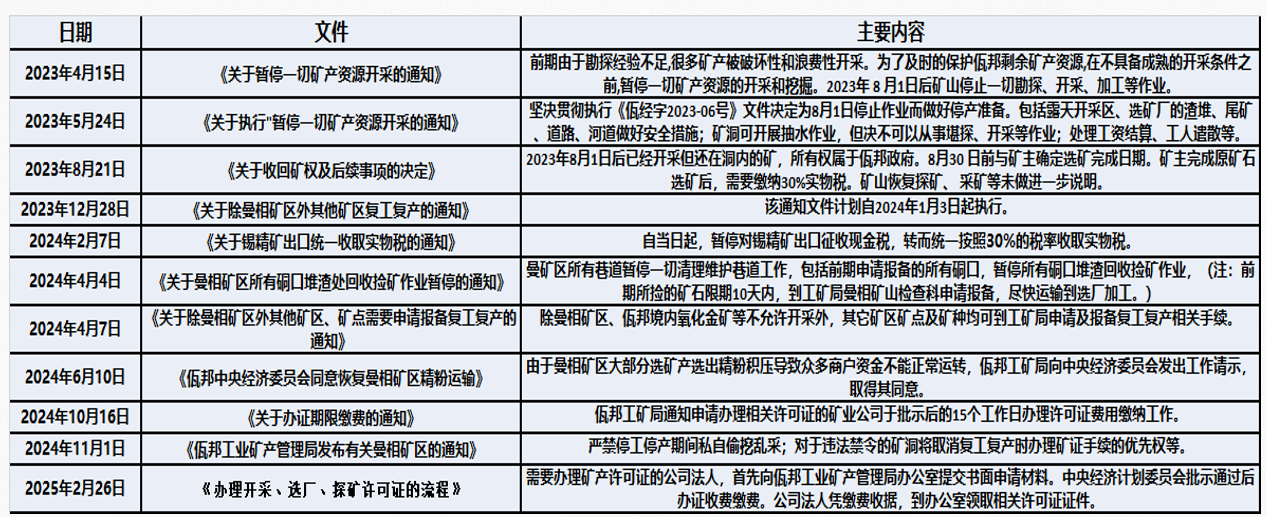

Wa State Export Policy

Myanmar Tin Ore Supply and Global Share

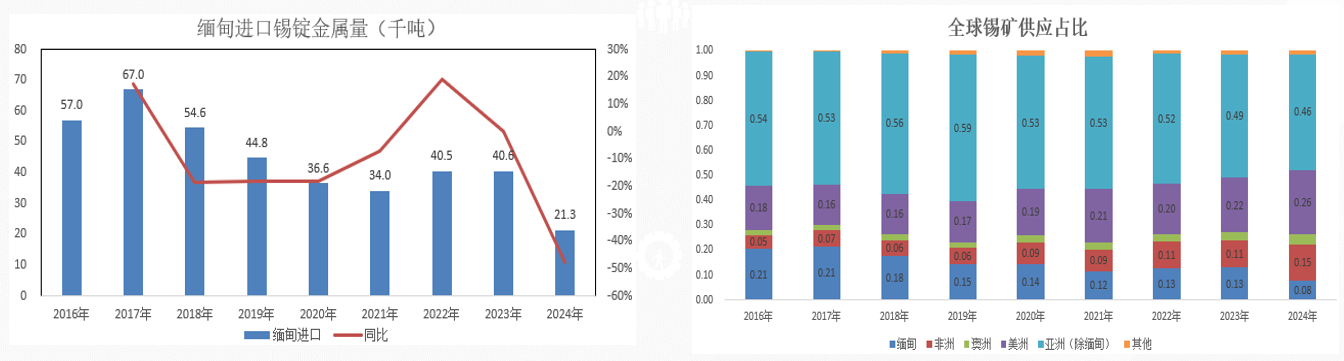

In 2024, Myanmar imported 21,300 mt of tin ingot metal content, a YoY decrease of 47.54%. By April 2025, the imported physical content was approximately 3,600 mt, a YoY decrease of 20%.

Due to excessive mining in earlier years, the grade in Wa State has been declining annually. Coupled with policy changes in 2023, Myanmar's share in global tin ore supply has dropped to 8%, with Q1 this year further declining to 3%.

Current Market Status of Tin Mines in Wa State

Numerous Beneficiation Plants

Currently, there are approximately 30 beneficiation plants, with processing capacities ranging from 50t/d to 3000t/d. Over 30% of these plants have a daily processing capacity exceeding 1000 mt.

Insufficient Ore from Mines

There are approximately 2 million mt of ore stockpiled at various locations, with varying tin grades. The overall grade is relatively low. Currently, most beneficiation plants do not have a significant amount of high-grade ore stockpiled. The low grade leads to high production costs, low production profits, and even losses.

Advanced Beneficiation Technology

Efficient mining equipment, such as large-scale excavation equipment, rock drilling jumbos, scrapers, and mining trucks, has been put into use. Advanced beneficiation plants have been constructed, with beneficiation technology even surpassing the general domestic level.

Numerous Mining Pits

According to incomplete statistics, hundreds of mining pits, both large and small, have been opened in the Mangxiang mining area. Currently, all mining activities have ceased due to the mining ban, and the maintenance costs for the pits are high.

Types and Costs of Tin Ores Imported from Myanmar

►Types of Concentrates

The tin ores exported from Myanmar to China at this stage: approximately 20% are flotation concentrates with a grade of around 10%, approximately 60% are gravity concentrates with a grade of around 17-18%, and approximately 20% are tin ores with a grade of around 20%.

►Cost of Tin Ores

Cost of tin ores = government taxes + beneficiation plant fees + logistics and transportation costs

Government taxes: include in-kind taxes (for ore with a grade higher than 20%) and cash taxes (for ore with a grade higher than 20%).

Processing fees at beneficiation plants: The average processing fee for raw ore is over 200 yuan/mt. Therefore, raw ore with a grade of around 0.8 is currently considered break-even ore, and only ore with a grade above 1% will generate a small profit.

Reagent costs: Based on the reagent costs used in the beneficiation process in recent years, as the reagents are entirely imported from China and the grade of raw ore is declining, reagent costs will gradually increase. This will also be one of the main reasons for the increase in the cost of Myanmar's tin ores.

Tin Ore Market and Policies in Myanmar

►Tin Ore Export Situation

Export requirements have become increasingly stringent. On one hand, this is reflected in the logistics load restrictions. Additionally, there are only over 40 units in the transportation fleet, and other types of ores are also shipped simultaneously, leading to a shortage of trucks.

On the other hand, it is reflected in the lengthy process required for customs to handle export documentation. Previously, export companies conducted their own sampling and testing for customs declaration. Now, the Yunnan Customs strictly implements the cargo import policy. Exporting tin ores requires prior appointment with the customs, followed by arrangements for the quality inspection department, ore supply bureau, customs department, etc., to be present for sampling and testing.

Resource Situation in Southern Myanmar

Resource Situation in Southern Wa State: There are abundant tungsten-tin deposits in southern Myanmar, with three major ore concentration areas from north to south: Pinlaung, Tavoy, and Myeik.

The Mawchi tin mine, located in the Pinlaung ore concentration area, is a world-class tin-tungsten deposit with an estimated ore reserve of 350,000 mt. Before World War II, it was the largest deposit globally. However, due to war damage and declining ore grades, it has now shifted to artisanal mining, with an annual production of less than 100 mt.

The Tavoy ore concentration area currently mines around 400 mt of tin ore, most of which is transported to Thailand for smelting.

The Tanintharyi mining area, located in the southern part of Wa State, has an annual production of around 400 mt, primarily from small and medium-sized mines.

Resource Situation in Southern Myanmar

It provides an introduction to the resource situation in southern Myanmar.

Imports in the South, Earthquake Impacts

Analysis of Tin Ore Imports in Myanmar

►Decline in Mine Grade, Reduction in Proportion of Myanmar Tin Ore Imports

Since 2012, Myanmar has been an important source of tin raw material imports for China, accounting for over 80% of imports. The volume exported to China has increased year by year, peaking in 2016 with imports of 474,600 mt physical content of tin ores and concentrates. Since then, it has declined annually, with the grade of Myanmar tin ore also dropping from an initial 10% to only 1%-2% currently.

Underground mining has increased mining difficulty and costs. After moving to low-altitude areas, a significant amount of ore has shifted to sulfide ore, with high temperatures and hot water posing major challenges, leading to a noticeable reduction in ore production. Since 2018, Myanmar's tin ore production has shown a clear downward trend.

►Myanmar's Mining Ban Raises Market Supply Concerns

In late April, the Wa State government in Myanmar announced a policy to halt all exploration, mining, and processing operations at mines after August 1, 2023. Previously, China relied heavily on Myanmar for tin ore imports, with the proportion consistently maintained at over 75%. Currently, beneficiation plants are gradually resuming operations, and production is expected to rebound. However, the key focus remains on when the mines will resume production.

Summary and Outlook

This analysis combines the production, processing, logistics, transportation, and investment environment in Myanmar.

Wa State Area: Currently, beneficiation plants in the Myanmar region are gradually resuming operations, but the timing for mine resumption remains uncertain. The area has a large inventory, but the ore grade is not high, and processing costs are relatively high. Therefore, the current unit price is not enough to support production costs across various aspects, and the impact on raw materials is significant. If the rectification in the Wa State area is completed with good results, the grade of raw ore in the area may improve, and processing difficulty may decrease accordingly.

Southern Mining Areas: In areas such as Loikaw and Tavoy, a few plants have just begun to gradually resume production. Due to unstable situations and the ongoing rainy season, transportation difficulties persist, and essential production materials cannot be purchased in a timely manner, leading to a temporary halt in production.

Africa is one of the main drivers of future tin ore production growth, with a gradual increase in production observed after 2018. In recent years, as the region has continuously improved the level of production mechanization, moving from traditional manual or small-scale mining, tin ore production has increased year by year.

Finally, it provides a brief introduction to Gejiu Qiandao Metals Co., Ltd.

》Click to view the special report on the 2025 Indonesia Mining Conference & Critical Metals Conference

![The Most-Traded SHFE Tin Contract Opened Lower and Then Traded Stronger, Spot Market Recovers Amid Downtrend [SMM Tin Midday Review]](https://imgqn.smm.cn/usercenter/WWXJU20251217171753.jpg)

![The most-traded SHFE tin contract fluctuated rangebound during the night session, with downstream enterprises mostly following up with small-lot transactions. [SMM Tin Morning Brief]](https://imgqn.smm.cn/usercenter/bYFQn20251217171752.jpg)